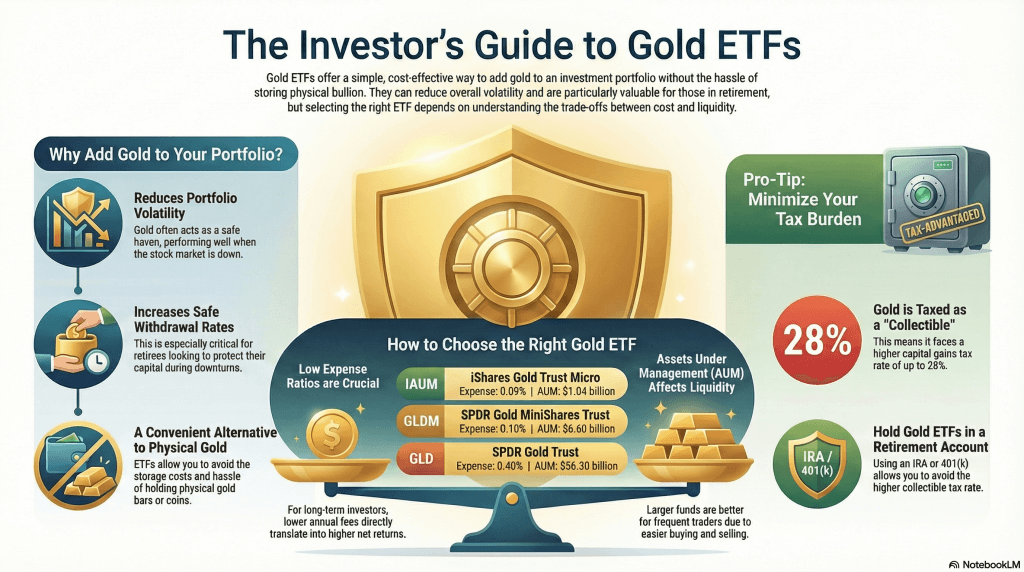

Retail investors can avoid the hassle and expense of holding physical gold bullion or gold bars by owning it indirectly via physical gold exchange-traded funds. For many, this can be an efficient and cost-effective way to hold gold in a portfolio.

Holding the right proportion of gold in a balanced investment portfolio can reduce overall portfolio volatility and in turn increase the safe withdrawal rate.

The chart below lists nine of the best gold ETFs ranked in order from the lowest to the highest expense ratio. Since their valuations all fluctuate with gold prices, the difference in returns between them will typically be driven by the expense ratio. The lower the expense ratio, the higher the return, and vice versa.

| ETF ticker | ETF name | Company | Inception | AUM *(billions) | Exp% (from low to high) | 2022 – 2023 CAGR** |

|---|---|---|---|---|---|---|

| IAUM | iShares Gold Trust Micro | Blackrock | 2021 | $1.04 | 0.09% | 6.10% |

| GLDM | SPDR Gold MiniShares Trust | State Street Global Advisors | 2018 | $6.60 | 0.10% | 6.07% |

| SGOL | abrdn Physical Gold Shares ETF | Abrdn Plc | 2009 | $2.82 | 0.17% | 6.03% |

| BAR | GraniteShares Gold Trust | GraniteShares | 2017 | $0.97 | 0.175% | 5.99% |

| AAAU | Goldman Sachs Physical Gold ETF | Goldman Sachs | 2018 | $0.62 | 0.18% | 6.01% |

| IAU | IShares Gold Trust | Blackrock | 2005 | $26.69 | 0.25% | 5.89% |

| OUNZ | VanEck Merk Gold Trust | VanEck | 2014 | $0.83 | 0.25% | 5.95% |

| GLD | SPDR Gold Trust | State Street Global Advisors | 2004 | $56.30 | 0.40% | 5.75% |

| PHYS | Sprott Physical Gold Trust | Sprott | 2010 | $6.67 | 0.41% | 5.32% |

**Don’t expect these returns every year. The point is to show how the returns generally go inverse to the expense ratio.

Expense ratios

As you can see from the above chart, the expense ratios of these 9 ETFs range from 0.09% to 0.41%. That is a significant range in cost!

The two large players, Blackrock and State Street Global Advisors, are battling it out on their low cost micro share ETFs, with IAUM currently edging out GLDM by 0.01% (0.09% expense ratio vs 0.10% expense ratio).

Both of these choices are quite a bit lower in cost than each of their primary and more well known gold ETFs (IAU and GLD).

Fees make a big difference in investment returns for the long term investor, as described in this Investopedia Article.

Assets Under Management (AUM)

As you can see from the chart above, State Street’s SPDR gold shares (ticker GLD) is the largest gold ETF at over $56 billion. Blackrock’s IAU comes in second at approximately $27 billion. These funds are quite large in comparison to their lower cost options mentioned above (IAUM & GLDM), with AUMs of between $1 billion and $7 billion.

Why does this matter? For investors holding gold ETFs for the long term as part of an overall portfolio, it likely won’t. For those trading gold on a regular basis, it will. This is because the larger funds will often have much more liquidity, resulting in better transactional pricing due to a tighter bid / ask spread.

For those trading gold quite a bit, such as institutions, better pricing due to a tighter pricing spread may offset the higher expense ratio. For long term buy and hold investors, it probably won’t.

Why hold Gold funds?

For someone in the accumulation phase, which means they are adding to their investment portfolio and not yet drawing down for a number of years down the road, gold usually won’t add much value.

This is because gold historically has lower returns over time than equities.

However, for someone in the withdrawal phase (financially independent or in retirement), holding the right amount of gold can provide substantial value to a properly balanced risk parity portfolio by reducing volatility and increasing the safe withdrawal rate. Some of the common risk parity portfolios will contain 10% – 15% gold in addition to the right balance of other asset classes. Obviously this is a personal choice based on your investment objectives, risk tolerance, and the other components in your portfolio.

The reason for this is that gold often does well during times of economic turmoil and fear. In other words, when the stock market is tanking, gold will often be seen as a safe haven, which can give it a low correlation to equities when you desperately need it.

You can read more about using gold as a hedge here.

For someone trying to have the best safe withdrawal rate in retirement, gold can be a critical component. You can read more about that here.

What about gold mining stocks?

From my seat, holding gold mining stocks defeats the purpose of trying to hold gold as a portfolio hedge.

When you invest in the gold mining industry, you are now mixing the performance of the commodity with that of a company, which can yield dramatically different results.

For example, mining companies (just like any other company) can perform poorly for many reasons that have nothing to do with the commodities they are handling. There could be lawsuits, market consolidations, labor issues, and a myriad of other variables than can impact a company’s performance.

If you are holding gold in a balanced portfolio as a hedge against bad economic events, you don’t want to water down that hedge by holding a company whose results might be quite different than what you were expecting by holding Gold in the first place.

What about Institutional Risk?

Investing has risks. One of them is institutional risk. What would happen if the investment firm had some type of fraud, went bankrupt, or if the physical gold was stolen?

If you hold gold indirectly via an ETF, SIPC insurance should apply up to the allowed limit, typically $500,000. This should cover you against an investment firm fraud issue. Other insurance and obligated parties may also apply regarding the storing of physical gold owned by the ETF. Be sure to read the prospectus and do some due diligence on the provider to confirm.

You can read more about SIPC coverage on their website.

Regardless of insurance, it is a reasonable risk mitigation tactic to hold funds at more than one brokerage institution. For example, if one institution had a data breach, and accounts were inaccessible for a period of time, you would have access to your accounts at the other institution(s) while the breach issue was being sorted out.

Taxes and holding a physically-backed Gold ETF

Ideally you would want to hold a Gold ETF in a retirement account such as a 401K or an IRA.

The main reason is that you can avoid the higher capital gains tax rate (28%) that can apply to Gold as a precious metals commodity.

In addition, you can also avoid the hassle at tax time of having to report lots of de minimis sale transactions, as many funds need to sell small fractions of your shares each month to cover the fund expenses. These often do not have a material tax impact, but your broker is required to report all of these sales on a 1099-B for taxable accounts at year end, which in turn needs to get on your tax return.

For example, if you hold a gold ETF with $10,000 invested for an entire year, you will likely get a 1099-B at tax time with 12 sale transactions on it, showing one each month. Each sale would often be just a few dollars, but it still needs to be reported.

Remember that in a retirement account, there is no 1099-B reporting by the broker for investment sale transactions, as your transactions are not included for tax purposes as long as the funds stay in the retirement account. You can read more about the tax impact of holding investments here.

The problem for many investors that want to hold some Gold in their portfolio as a hedge is that many 401K retirement plans limit investor choices. That is unfortunate since most people have a significant amount of their investments in retirement accounts.

With an IRA, you don’t have restrictions on which ETFs you can purchase. If that is not an option, then you will have a standard brokerage account as an option as well, but you’ll have to deal with the tax implications noted above.

How to Buy Gold ETFs

Buying an ETF is just like buying a stock.

You will need to go into your brokerage account and place a trade for the number of shares you want to buy.

You can place a market order (you get the next available price) or a limit order (you put a restriction on how much you are willing to pay).

Once the trade executes, you will own the shares.

Disclaimer: Investing has the risk of loss. Past performance is no guarantee of future results. Be sure to understand all the risks before investing. You should understand and evaluate your risk tolerance. Read the prospectus. Validate data from multiple sources and do thorough research before making any investment decisions. If you decide to use a financial planner for investment advice, be sure to use a Fee-Only Financial Advisor that is a Fiduciary, which legally obligates them to do what is in your best interest and not theirs!

Infographic

Executive Summary: 9 low cost physical gold ETFs for portfolio parity

- Investing in ETFs that hold physical gold as its underlying asset is a convenient way to have exposure to the gold market in your portfolio without managing and holding gold coins or bars yourself.

- Above are nine of the larger, low expense ratio physical Gold ETFs offered in the marketplace

- The annual fees of these nine gold exchange traded funds range from 0.09% to 0.41% per year of assets under management

- As shown in the chart above, the comparable returns between these ETFs are driven by the spot price of gold, net of the fees

- The large funds will typically be more liquid and have better bid / ask spreads than the smaller funds

- Gold may not add much value for an accumulation portfolio, but for those in retirement, the right proportion of gold can be an important holding

- Gold mining stocks are an option chosen by some, but their results can be wildly different than what you would expect by holding the precious metal itself

- Institutional risk exists for all investing. SIPC and other insurance can alleviate some of those concerns.

- Gold has a higher capital gains rate and often more tax reporting obligations due to fund share sales needed to pay fees, which makes holding these ETFs in a retirement account often preferred.

- You trade these ETFs on stock exchanges just like with stocks or other ETFs, by placing trades via your investment trading platform