Both have Pros and Cons. Let’s review and discuss options.

Heloc

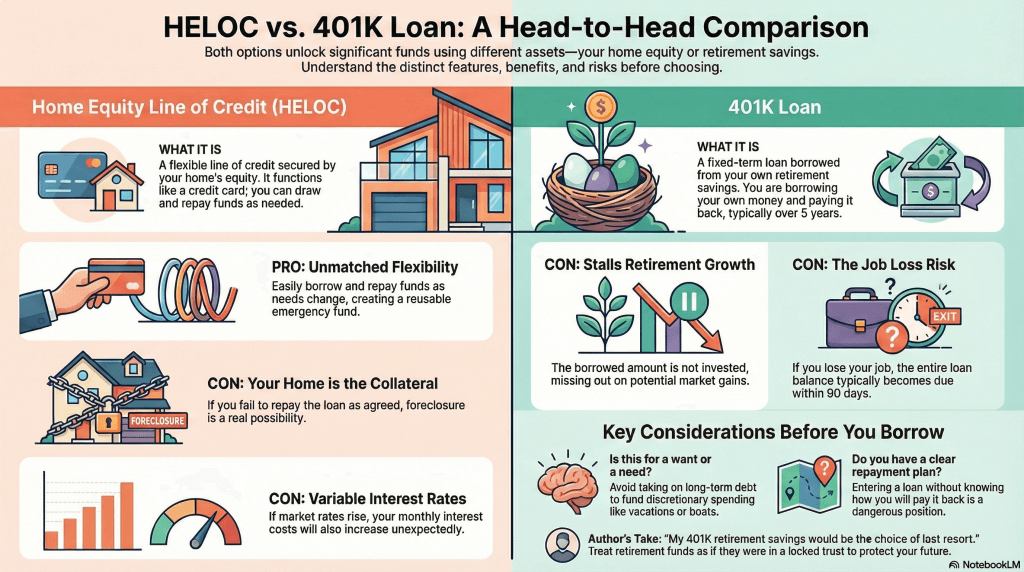

A Heloc stands for Home Equity Line of Credit. Once approved for a Heloc loan, you can draw and paydown as you please. Typically this will be an adjustable interest rate loan that will reset monthly.

In order to get a home equity line of credit, you will need to go through an underwriting process at your bank or credit union. To qualify for the line of credit, you will need to have adequate equity in your home as well as sufficient income as required by the bank. They will also likely pull your credit report to review your credit score in order to conclude that you are a low risk borrower. The amount you could get approved for will ultimately be based on the equity you have in your home. In order to validate that, the bank or credit union will often order an appraisal to confirm the value of your home.

The bank will record a mortgage lien on your property. The amount will be based on the amount you have been approved for. For example, if you are approved for a $70,000 Heloc, the bank will record that lien so that its position is secured.

Since you can draw funds at any time by writing checks or transferring funds, your actual loan balance could fluctuate quite a bit. The interest will be calculated based on your average outstanding balance for the month.

The interest charged for the month would typically be the minimum payment required for the month. In other words, you could just make interest payments to maintain the line. That being said, you will need to be diligent to pay down principal in order to prevent from being in debt perpetually. The bank would love that!

401K Loan

Most 401K plans allow you to borrow a lump sum of money from your retirement funds. These are typically fixed rate loans with payments over a 5 year period.

In other words, you are borrowing your own money and paying it back over time with regular monthly payments.

In order to borrow funds, you will need to complete paperwork with the plan administrator or human resources department. Once you determine the amount, the full amount will be pulled out of your retirement funds and deposited into your bank account.

You will then be responsible to make the monthly payments on time during the repayment period to keep your account in good standing.

Why are you borrowing?

What is driving the need to borrow funds? There are many different reasons that may create the need.

The amount and necessity is a key question to help make the borrowing decision.

If it’s to fund a vacation or other discretionary spending such as buying a boat, please think twice. Actually no, think three times! These items are pure consumer spending that you should avoid taking on long term debt to fund. These payments will stick around long after the memory of the trip or purchase fades.

If it’s for a home improvement or addition, it typically won’t have a dollar for dollar payback, but you should get a partial recovery of your investment in an appreciating asset (you home).

There are obviously lots of reasons in addition to these examples that could drive the need to borrow. Everyone has their own unique financial situation to manage.

At the time of borrowing you should have a plan as to how and over what time period you are going to pay it back. If you have no idea how you are going to pay back the loan, that is a dangerous position to put yourself in.

Heloc Risks

When you borrow from the equity of your home, you are putting up your home as collateral for the loan. That means your house is now at risk. If you fail to pay back the loan as agreed, foreclosure is always a possibility.

401K loan Risks

Borrowing from a retirement account is a very serious thing. Your retirement savings should be one of the last options used to borrow money.

If you are on a 5 year repayment plan, that is a long time for funds not being invested in the stock and bond markets. You will lose the magic of compounding over those years. Yes the market could go down, as well as it could go up.

Regardless, the market has proven to increase over time and the more years you are not invested, the lower your future balance will likely be. You may have to work extra years on the back end to make sure your retirement is set, and borrowing from your retirement plan could be one of the contributing reasons.

If you fail to pay back the 401K loan as agreed, you could be in a “deemed distribution” situation. What that means is that if you don’t pay the money back, you have essentially permanently pulled money out of your 401K plan early. That deemed distribution will show up as a 1099-R at the end of the year and you will be responsible for paying income taxes and possibly the 10% early withdrawal penalty (depending on your age). Ouch!

Heloc Pros and Cons

The Pros of the Heloc are as follows:

- Flexible line of credit lets you borrow and repay easily as your funding needs change

- Having the line gives you the option to borrow in the future should another need arise, acting like an emergency fund

- If you have a lot of equity in your home, you will qualify for larger amounts

The Cons of the Heloc are as follows:

- Your house is at risk by adding an additional mortgage to your properly

- The interest rate is typically variable, which means if rates go up your monthly interest costs will go up too

- There will be a credit check and underwriting process to go through, which makes it slower and more expensive to get funded

401K Loan Pros and Cons

The Pros of a 401K Loan are as follows:

- Should be much faster to get the loan than a Heloc. No underwriting is needed.

- You will get a fixed rate of interest so no surprises as with a variable rate

- Borrowers are provided with fixed repayment schedules

The Cons of a 401K Loan are as follows:

- The max you can borrow is the lesser of 50% of your vested balance or $50,000

- Your loan amount is no longer invested in stock market mutual funds or other investments, which inhibits portfolio growth

- Many plans won’t let you contribute to a 401K if you have a loan outstanding, which further limits your retirement savings

- If you have a job loss with your employer the unpaid balance on your loan will typically become due within 90 days or less, yikes!

- You can only borrow from the 401K at your current employer (no legacy 401K plans)

- If you default on the loan the unpaid amount will be considered a deemed taxable distribution and likely the 10% early withdrawal penalty in addition to federal and state income taxes

Other Options to Consider

You may have other options in addition to using a Heloc or 401K loan.

You could go with a standard home-equity loan, rather than a home equity line of credit. A home equity loan would be for a fixed dollar amount. It won’t flex like a Heloc where you can paydown and draw again. However, the advantage would be the fixed interest rate rather than a variable interest rate on a Heloc. In other words, you will have a stable payment and payback period with a home equity loan.

Some people might choose to do a cash out refinancing of their primary mortgage loan. For example, if you had a $100,000 mortgage loan outstanding and your home was worth $220,000, you would have $120,000 of equity in the home. In this case you could refinance your mortgage, for example, to increase it from $100,000 to $150,000, which would result in a $50,000 cash out. With this type of a refinance, you would be spreading out the payment over a longer period of time. That may or may not be the right think to do!

A personal loan would be another option. You could go to your bank or credit union and request an unsecured loan. The interest rate would likely be higher since it’s unsecured (no collateral like a home), which means you would need a good or excellent credit in order to be approved.

What to Avoid

Please avoid using a credit card to fund higher dollar amount needs. Credit cards, of course, have much higher interest rates and compound very quickly.

You can play the game of doing balance transfers to other cards with 0% promotional offers, but that game can end quickly. Also read the fine print for balance transfer fees too. Those can get expensive!

Time to Make a Decision

Borrowing money from your home equity is a big deal. Borrowing money from your retirement plan is a REALLY big deal.

Don’t make this decision lightly. The sour taste of having to make loan payments month after month after month will last long after the sweetness that the original borrowing provided.

If you are not comfortable making the decision, don’t rush it! It would probably be a good idea to discuss the decision with a trusted financial planner or a financial advisor. You need to determine that the repayment terms work with your budget.

Just because the bank or 401K plan administrator says the loan works for them, doesn’t mean it works for you! You are the one that has to make the loan payments, not them. Don’t get pushed into loan terms you are not comfortable with! YOU are the one that has to live with it.

What would I do?

Everyone has their own level of risk and level of comfort given these loan options. For me, my 401K retirement savings would be the choice of last resort. I personally would not want to impact my future retirement by borrowing money from my 401K retirement savings account. To me that money should be treated as if it was in a locked trust, with no way to access. That line of thinking forces me to find another less invasive solution.

I personally feel that a home equity line of credit is a better option. I have used home equity lines of credit at various points in time over the years. They have come in handy for larger home renovations and other temporary credit needs. There is cost and time invested to set one up, but once you have it you get the flexibility of borrowing and paying back as needed. Once paid off, that line of credit is available as a safety valve should there be an unexpected future need. To maintain the line you typically would need to pay a nominal annual fee to keep it active (ie: $50 per year or something similar).

But enough about my thoughts. Hopefully you now have enough facts to make an informed decision based on your own situation.

Infographic

Summary: Home equity line or 401K Loan: which is better?

- Borrowing from a Heloc or your 401K is serious business

- Reconsider why you need to borrow and if there are other options to handle your situation

- The main benefit of the Heloc is that it is flexible, allowing you to borrow and repay as needed

- The main benefit of the 401K loan is that it has a fixed payment and no underwriting

- The main disadvantages of a Heloc is a variable interest rate and the slow and more costly underwriting process

- The main disadvantages of a 401K loan is the limited borrowing amount and the loss of investment compounding for the loan balance amount