VTSAX and FSKAX are total U.S. stock market index funds offered by two investment giants, Vanguard and Fidelity.

VTSAX = Vanguard Total Stock Market Index Fund Admiral Shares

FSKAX = Fidelity Total Market Index Fund

Chart comparing VTSAX vs FSKAX

| Category | Vanguard Total Stock Market Index Fund Admiral Shares | Fidelity Total Market Index Fund | Comments |

|---|---|---|---|

| Ticker symbol | VTSAX | FSKAX | V=Vanguard F=Fidelity |

| Company | Vanguard | Fidelity | Two large reputable companies |

| Structure | Index mutual fund | Index mutual fund | Both are index mutual funds |

| Net asset value | $323.9 billion | $78.9 billion | As of 11/30/23; Both are very large |

| Index used | CRSP US Total Market Index | Dow Jones U.S. Total Stock Market Index | Both aim to cover the entire US stock market |

| Fund weighting | Cap weighted | Cap weighted | Both funds are market capitalization weighted |

| # stocks held | 3,761 | 3,908 | Holdings as of 11/30/2023 |

| Composition | Equity – US Stock Market | Equity – US Stock Market | No material difference |

| Management needed | Passive | Passive | Both index driven – active management not needed |

| Investor trading | End of day | End of day | Mutual funds trade at the next end of day closing price |

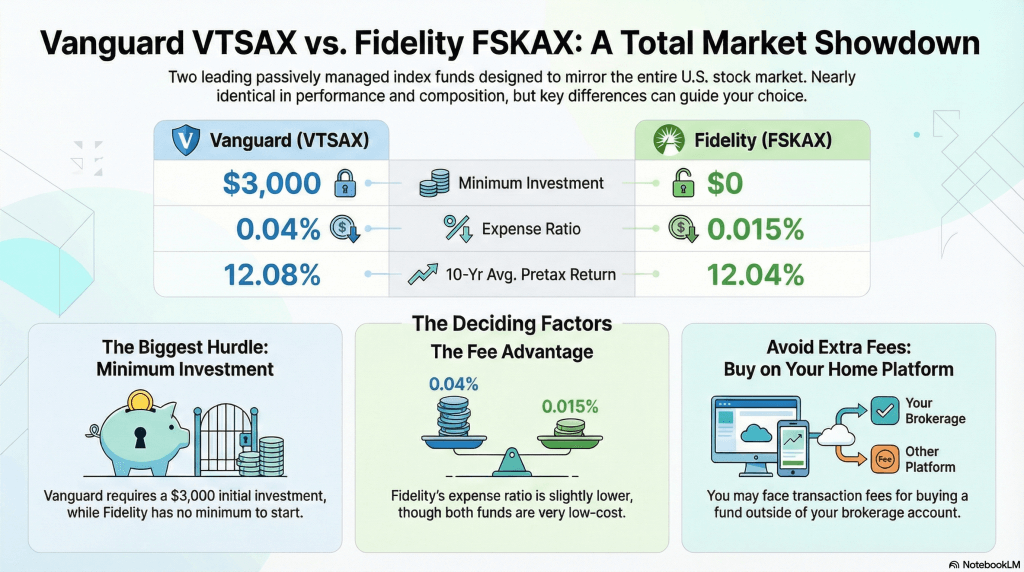

| Initial investment | $3,000 | $0 | Fidelity has no minimum initial investment |

| Fund expense ratio | 0.04% | 0.015% | Fidelity has a lower expense ratio |

| Capital gain distributions annual tax cost | 0.50% last 10 year average | 0.52% last 10 year average | Vanguard is 0.02% lower |

| Average pretax return for the 10 years ending 12/31/2022 | 12.08% | 12.04% | Vanguard is 0.04% better based on the last 10 years ending 12/31/2022 |

| Summary | U.S. equity coverage at a low cost | U.S. equity coverage at a low cost | Both funds offer good coverage of the US Stock market at a low cost |

Key Differences

The primary difference between the two funds is that Fidelity has no minimum initial investment and Vanguard has a $3,000 minimum initial investment. Subsequent investments can be any amount for either fund, so there is no difference once the initial investment occurs.

The other differences that would often be a deciding factor are quite small. The expense ratios, average returns, and the capital gain distributions annual tax cost are so close that they don’t have much of an impact on the decision making process. See the chart above for the specifics.

Be Careful of Transaction Fees

If your account is with Fidelity Investments and you want to buy the Vanguard VTSAX fund, you may incur an additional transaction fee to do so. Since these funds are so similar, you would likely be better served to buy the Fidelity FSKAX if you are buying from your Fidelity account. The converse would apply to Vanguard if you want to purchase the Fidelity fund.

Fund Tax Efficiency

If you hold one of these funds in a retirement account (401K, IRA, Roth IRA, etc), the fund tax efficiency is irrelevant. Remember that in a retirement account, tax is not an issue until you take money out of your account. Trades or distributions within the account will not have a tax impact.

In a taxable account, the fund tax efficiency does matter. Mutual funds will issue 1099’s at the end of the year to taxable accounts for the capital gain distributions that are passed on to the fund holders. As you can see in the chart above, this annual cost has averaged between 0.50% – 0.52% for two funds over the last 10 years ending 12/31/2022. You can see the specifics on this by reviewing the fund prospectus.

To dive deeper on the tax impact of various accounts, read this article.

Cap Weighted Funds

Both funds are market capitalization weighted, which is a common structure. What this means is that the thousands of individual stocks held in the fund are not held in equal weight, but instead by their individual market value. The market value of a stock equals the total shares outstanding times the market share price.

So, a large company will have a larger percentage of the fund assets than a small company. This would be proportional to the overall market as well. These total market index funds will often perform very similarly to an S&P 500 index fund, which is a fund of the largest 500 companies. This is because these U.S. total stock market funds are more heavily weighted toward large-cap stocks.

Year-to-date returns

As shown in the chart above, the annual returns over the last 10 years between the two funds are almost identical (12.08% vs 12.04%), which is expected given that their composition is very similar.

To review the investment performance by year you can go directly to the Vanguard website or the Fidelity website as provided by these links.

You can also see other details, as well as links to review the detailed investor prospectus.

Low Fees

Both of these funds have low fees. Vanguard’s VTSAX has an annual fee of 0.04% and Fidelity’s FSKAX is even lower at 0.015%. Both funds are quite a bit lower than mutual funds offered elsewhere.

Fees make a HUGE difference in your investment results over time. A fee of 0.50% to 1.0% doesn’t sound like much but the compounding impact over time is massive!

You can read more about the impact of a high fees on your returns in this Investopedia Article.

In the case of these two funds, however, the fees are so minuscule that the fees will not be an issue with either investment choice.

One of the reasons for the lower expense ratio is that these are both passive index investments as opposed to an actively managed investment. A passive investment that follows an index (in this case the US stock market) does not require the costs associated with active investment management.

In other words, you don’t need investment managers to make decisions of what investments to buy and sell as the index determines that automatically.

Before investing, be sure to check the latest expense ratios (see the links provided in this article), as they can change over time.

Infographic

Executive Summary: Fund Comparison: Vanguard VTSAX vs Fidelity FSKAX

- The main difference is that Fidelity has no initial investment minimum, whereas Vanguard has a $3,000 minimum investment

- Both funds have a very low expense ratio, which is very important, as a higher fee can have a major impact on investment returns over time

- The tax efficiency of the both funds are almost identical (0.50% vs 0.52% on average over the last 10 years)

- You may be best served buying the fund with the company that holds your account, in order to avoid a transaction fee for buying the competing product

- The funds have similar returns over the last 10 years, since their investment composition is almost identical

- Both index funds are cap weighted, which means the larger companies contain a larger percentage of the fund

- The total net assets of both funds are in the billions, which shows their popularity among individual investors

- Both funds are great option for long-term investors who need a low cost diversified portfolio of the entire stock market

- There is a slight difference in the benchmark index for these different funds, but they are extremely close and they both mirror the total U.S. stock market

Disclaimer: Investing has the risk of loss. Be sure to understand all the risks before investing. Read the prospectus. Validate data from multiple sources before making any investment decisions. If you decide to use a financial planner for investment advice, be sure to use a Fee-Only Financial Advisor that is a Fiduciary, which legally obligates them to do what is in your best interest and not theirs!

Articles to Read

- Do I pay taxes on stocks even if I don’t sell them?

- Total Stock Market Fund VTSAX vs S&P500 ETF VOO

- Can I invest $20 in the stock market now?

- Difference of a Fee Only vs Fee Based Financial Advisor

- Best Small Cap index ETFs to compliment your Equity portfolio

- How to build the Coffeehouse Portfolio with ETFs