Your expected longevity is a critical component to your retirement planning. If you are married, the combined life expectancy with your spouse will be even more important.

Rather than just picking a life expectancy age such as 80, 85, 90, etc., why not spend a few extra minutes to look at the actuarial probabilities and plan around that instead?

No one wants to run out of money in retirement, so addressing the life expectancy variable in more depth is worth the extra effort.

Actuaries Longevity Illustrator (ALI)

There is a free web-based tool called Longevity Illustrator that will give you both individual and joint longevity reports. All that you need to do is enter some basic information, which takes less than a minute.

The site is quite intuitive and easy to use. It was created jointly as an educational tool by the American Academy of Actuaries and the Society of Actuaries.

The information you provide can be generic. You don’t need to provide your real name or birth dates if you don’t want to. You can use the first day of your birth month as your birth date, for example.

In order to get the reports you just need to answer the following questions for you and your spouse (if applicable):

- First Name (or whatever you want to put here)

- Date of Birth (so it knows how old you are)

- Retirement Age (so it knows how long of a retirement you will have)

- Gender (important for the mortality tables)

- Do you smoke (obvious impact on mortality)

- General Health (poor, average or excellent – also impacts mortality)

Below is a sample of the data I entered as an example. I put in a husband and wife at age 55 currently, with plans to retire at age 65.

They are both in excellent health and do not smoke.

That’s it. It just takes a few simple steps and a minute of your time.

You then just click the “View Results” button. The tool quickly generates a few easy-to-read charts and graphs.

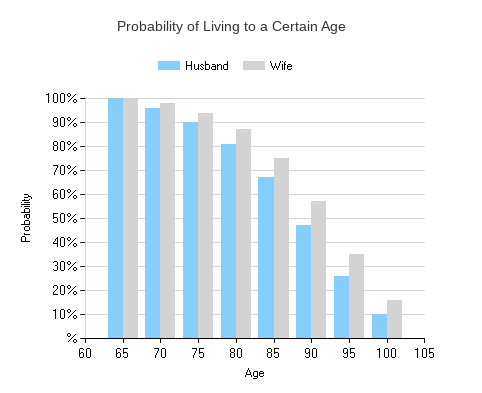

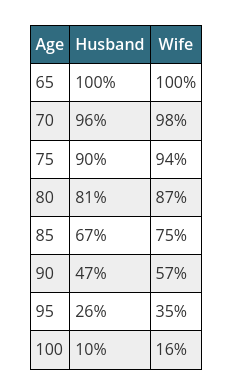

Report 1 – Probability of Living to a Certain Age

The first report generated is the probability of living to a certain age.

This is a very helpful tool to help in financial planning in retirement. You can see that there are not a lot of variables that are used as inputs. Apparently these are the most critical ones to get a reasonable handle on the probability of living to a certain age.

For example, your general health status has a relatively big impact. I ran the tool using both excellent health (chart below) and average health. The probability of the wife living to age 90 decreases from 57% to 49% just by changing that one health variable.

You can easily click the “modify data” button to go back and make changes to the data you entered. This will allow you to see how some of the variables impact your life expectancy.

Your financial advisor will often call the age you expect to live as your “planning date.” With this process you normally pick an age and then the Monte Carlo simulations are run to see if your financial needs will be met until your planning date given your retirement savings, investment strategy, expected social security benefits and anticipated income from other sources such as a pension.

For example, the Monte Carlo simulation might say that you have an 85% chance of success of your money lasting until age 90 (planning date) given all of the planning variables you provided.

This tool can help you pick a date that you are comfortable planning around. See below for the graph and chart regarding the “Probability of Living to a Certain Age” using the inputs I provided above.

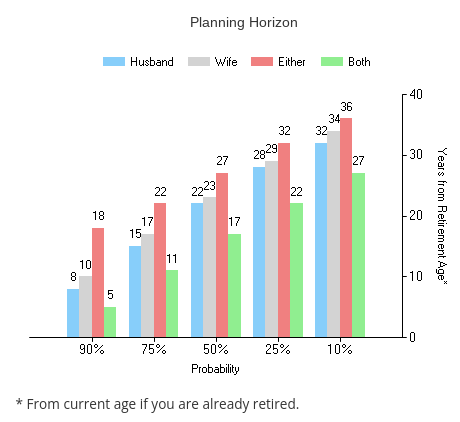

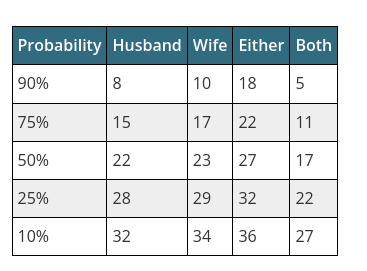

Report 2 – Planning Horizon

The second report provided, called “Planning Horizon,” might be even more useful for retirement planning purposes.

This report shows how many years you, your spouse, and either one of you or both of you would likely live in years after your retirement date. The report has a full narrative as well as a graph and chart.

Given the data entered in the example above, here is the graph that was generated:

I like the narrative and guidance the report also provides. For example, the narrative explains that a reasonable plan would likely be to plan to the 25% probability level. In that case, It is likely the husband and wife will live 28 and 29 years, respectively, in retirement.

In addition, there is also a 25% probability that you both will have 22 years in retirement (both surviving) and 32 years in retirement that at least one person will still be living. This data can help you plan for how long your money needs to last. In this case, your money needs to last up to 32 years after retirement to cover 75% of the probabilities.

Here is the same data in chart form. It shows the probably and number of years the husband, wife, either or both will likely live after the retirement date entered at the beginning of this article.

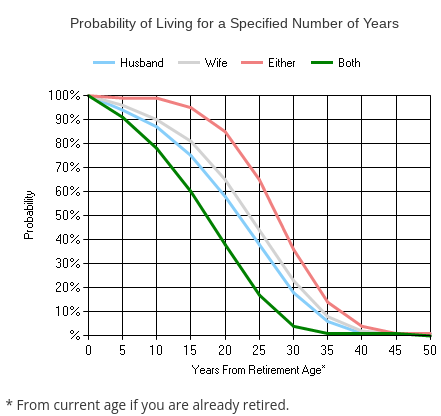

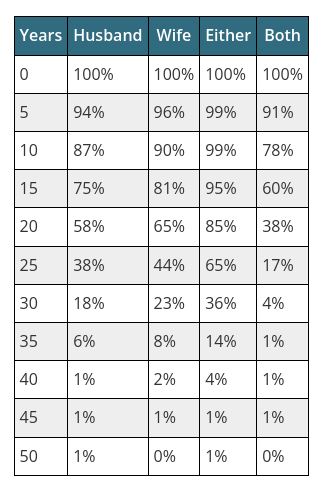

Report 3: Probability of living a Specified Number of Years

This is the last report. It is a spin-off of report 2. It provides the longevity data from report 2 in a different format.

First, instead of a bar chart, it shows a line graph. This gives you a better feel for the steepness of the curve, and might be easier to understand than the bar chart.

Here is the data chart. Again, it is just presenting the data differently than report 2. Instead of showing the probability % and then the number of years, it is instead showing the number of years and then the probability percentage.

Also a reminder that this data is using the inputs I entered in the tool earlier. Your results will vary depending on what you enter for the variables.

It’s an easy to use free online tool. Click this link: Give it a try right now!

Conclusion – Using the Tool

As you can see, this tool generates a lot of good information quickly. There are also helpful narratives that go along with the reports.

The site clearly explains that these reports provide general information given standard mortality rates based on the information you provided. Your personal health outlook, health family history and other variables related to your individual situation could make your own longevity quite a bit different than what is shown using this tool.

This type of tool is a very good start for planning purposes, which is better than just arbitrarily picking an age. You could provide this information to your financial planner to create a more fine tuned plan. Your longevity planning dates are needed for your financial plan.

Given your risk tolerance, you can decide how safe you want your plan to be. Being safer means adding additional years to your financial plan, which means you need a larger investment portfolio or other income sources to ensure your plan is good.

Getting a Financial Plan

When getting financial advice for financial planning, be sure to use a qualified financial professional that is a fee-only Fiduciary. Being a Fiduciary means that they are legally obligated to do what is in your best interest and not theirs.

Be careful as there are lots of financial people out there that are NOT fiduciaries. That means they might be more interested in selling you financial products that benefit them (commissions) or their firm, rather than you. Be sure to know the difference between a Fee-Only Financial Planner and a Fee-Based Financial Planner.

It is important to note that a plan is just a plan. It is not going to be perfect, as none of us have a crystal ball to exactly predict the future. However, having no plan is the worst case opposite position. Without a plan you are destined to fail for sure. The old adage that “if you fail to plan you plan to fail” holds true here.

It is okay for the plan to not be exact, as long as it is reasonably close to the actual results. If it is reasonably close you are likely going to be in good shape. You will have much better peace of mind if you use your best information to make a balanced decision.

Also keep in mind that a plan is as of a snapshot in time. Your plan and financial situation should be updated and reviewed periodically to make sure you are on course. If you deviate from the course, you then have an opportunity to make adjustments to get back on track before you stray too far off course. These periodic updates should occur even during your retirement years.

Infographic

Executive Summary:

- The jointly developed Actuaries Longevity Illustrator (ALI) is a free internet tool provided to anyone for informational purposes

- The professionals that developed the Illustrator website used their actuarial knowledge and back-end data source to create a useful tool that generates interesting results

- By going to the website and entering some basic information, you get three sets of narratives, graphs and charts

- The Illustrator’s results can be used to help guide you to set a longevity date to address the longevity risk in your financial plan

- Report 1 provides the probability of Living to different ages

- Report 2 gives you your planning horizon, which is a given number of years you and/or your spouse will likely live after your full retirement age

- Report 3 is a spin-off of report 2, which gives you the possible number of retirement years and related probability rather than the inverse of the related probability of retirement years in report 2

- When getting financial advisory services, be sure to use a Fiduciary who is legally obligated to look out for your best interest and not theirs

Note: all charts and graphs in this article are from the site LongevityIllustrator.org

A practical guide on using the Longevity Illustrator for retirement planning—insightful and user-friendly.